Latest topics

"Kim, CIPS, SWIFT, Easing up!" by ubiety 1/26/18

2 posters

Page 1 of 1

"Kim, CIPS, SWIFT, Easing up!" by ubiety 1/26/18

"Kim, CIPS, SWIFT, Easing up!" by ubiety 1/26/18

![]() by Ssmith Sat Jan 27, 2018 8:37 am

by Ssmith Sat Jan 27, 2018 8:37 am

Dinarians and exotic currency holders,

[Preface: Sorry in advance for typos and whatever else results from my haste. I'm trying to squeeze this in before an appointment in my actual business because the resistance among some exotic currency holders to very self-exposed help is troubling. I appreciate your indulgence.]

I realize fireswain [sic] is your new tech guru here in IDC, however, let's be clear, this person is a tech. She loves tech, she love to talk tech, she loves to impress with tech, but don't misunderstand - she is a tech not a designer of SWIFT, CIPS, or any of these long standing and fully public technologies.

Background on SWIFT, available to all of us:

SWIFT, or the Society for Worldwide Interbank Financial Telecommunication, is the world’s largest electronic payment messaging system, facilitating the exchange of more than $6 trillion a day, according to 2012 estimates. Though it gets lumped in with electronic funds transfer systems, it doesn’t do any of the funds transfers itself. In fact, it doesn’t even touch money. It does make money move by triggering the transfer mechanism between correspondent banks.

At its core, SWIFT is basically just a bank-to-bank messaging system. It supplies a standardized language that institutions use to communicate payment instructions and other info to each other. SWIFT messages are programmed in a language known as FIN. The system was designed and used to transfer messages between member institutions.

Before SWIFT, there was Telex. It’s helpful to start there, because rather than being created from scratch, the SWIFT system is rooted in some precedent. Telex—or the Teleprinter exchange, if we’re getting formal—was (and is) one of the original ways to transmit data developed during World War II. Though its roots were in the military, it was quickly adopted by financial institutions for their systems to communicate internationally.

By the 70s, Telex had gotten old: It was indisputably slow (transmitting bytes per second), lacked formatting standards (limiting the possibility to automate), and wasn’t as secure as evolving threats demanded (after all, it had basically become a directory served over the phone networks). Around the same time, domestic electronic funds transfer systems began to emerge, driven by a desire to eliminate paper from the payments process. (Imagine: the push to go paperless was a process that took shape in the 60s.) The distinction, of course, is that EFTs actually move money. But they often used Telex messages to get information about what needed to happen—which made the issues with Telex all the more pointed.

So in 1973, after a handful of studies and a lot of talking, a group of banks established SWIFT as a specialist’s alternative to Telex. They selected Brussels for the cooperative’s headquarters—evidently, choosing New York or London would have been too political. By the time SWIFT went live three years later, it comprised a messaging platform, a computer system to validate and route messages, and a set of message standards. More than 500 institutions from 22 countries were connected. Today, more than 11,000 institutions in more than 200 nations are connected to SWIFT. In 2015 alone, 6.1 billion FIN messages were sent through the network.

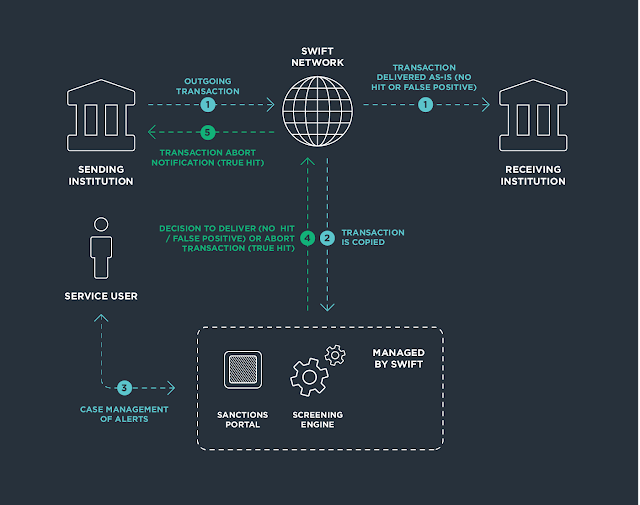

Here's a basic diagram on how SWIFT actually works.

SWIFT uses a system of codes to detail where a transfer is coming from, where it’s going, and how it’ll to get there. These strings of alphanumeric identifiers comprise an institution code, a country code, a location code, and a branch code. So in that way, it’s not dissimilar to the U.S. routing number system.

It’s worth reiterating that, because SWIFT doesn’t actually send money, institutions that use the network also need banking relationship to move funds. Each financial institution will have a dedicated SWIFT interface (in other words, a computer-based terminal) on-premises. Most banks set up their SWIFT systems so that they’re isolated from the rest of their networks. (Though, again, as we’ll cover later, not all do.)

Users can log in to these terminals to manually enter messages. Messages can also be auto-generated by the institution’s computer system and passed on to the terminal. The terminal then sends the SWIFT message to the regional processors in the sender’s country. The terminals only connect with processors through leased line, dial up, or public data network connections.

From there, the regional processor checks, stores, and forwards the data to its operating center, which passes the message on to the processor in the recipient’s country. That processor delivers the message to the receiver’s terminal, and then sends confirmation. Officials at the respective financial institutions are supposed to audit these to prevent fraud.

As indicated above, actually transferring funds internationally is a bank matter. Say two customers of the same bank are located in two different countries and want to transfer funds. The customer in country A will ask the bank to transfer funds to the customer in country B. Branch A will then tell its counterpart what to do via SWIFT. And then it’ll wire the funds and make the required book entries in its accounting system. That’s it. But it’s usually more complicated than that, and it often involves more financial institutions.

For example, if one financial institution doesn’t even have a branch in the beneficiary’s country, it might need to loop other institutions—in this context, called correspondent banks—to complete the transaction. If both banks (conveniently!) maintain accounts at a third institution, they might use that third bank to expedite things. They’d identify the relationship, send a secure message over SWIFT between the banks, and do a book transfer.

CIPS, also publicly available information:

One has to first understand the CIPS initiative before looking into how it works. The Cross-border Inter-bank Payments system is designed to facilitate financial transactions between different countries. To be more specific, the entire network settles cross-border RMB (Chinese currency) payments and trade for all of its partners. This means China is taking center-stage as far as this payments platform is concerned.

The development of CIPS dates back all the way to several years ago. After a few years of development, the first phase of CIPS was introduced to the rest of the world. The project gained immediate support from 19 Chinese and foreign banks, as well as 176 indirect participants across 6 different countries. At that time, some people saw it as a way for Russia and China to develop a payment system that could rival with SWIFT.

However, it appears that is not necessarily the goal, as CIPS signed a Memorandum of Understanding with SWIFT in 2016. To be more specific, SWIFT would be used as a secure and efficient communication tool for CIPS’s connection with established members. In a way, this is meant to allow cross-platform compatibility between different payment networks, as there is no reason to think CIPS wants to directly compete with SWIFT in the West.

It is also worth mentioning CIPS is not designed to facilitate funds transfer, as it is designed to send payment orders to be settled by correspondent accounts (keep this in mind every time you read someone talking about CIPS transferring money). This means partners of CIPS must have a banking relationship by either being a bank themselves or affiliating with an existing financial institution. It is not open to just anyone by any means, yet it aims to speed up cross-border payments by quite a margin. Or that is how it was supposed to go until things came to a change back in 2015.

To put this latter part into perspective, the CIPS protocol serves as a cross-border yuan trade deal tool instead of a network designed to facilitate capital-related transfers. Providing a unified network for settling deals in yuan sounds great on paper, yet the idea has suffered some setbacks in the past few years. The 2015 Chinese stock market crash has not helped matters either.

CIPS v SWIFT is about clearing – not investment money and it has no impact upon parking (i.e., storing or safekeeping) money. CIPS platforms which functions for the RMB, the same way SWIFT does for the dollar. Yet unlike the way SWIFT charges for swaps when nations have to use the dollar as a middleman since it still reigns as the world's singular reserve currency, CIPS allows for much lower transaction fees and the convenience of bypassing the U.S. currency through direct bi-lateral currency settlement. This doesn't mean CIPS actually transfers the money, it simply works more closely with the "member" institutions which effect the actual transfer.

"Direct bi-lateral currency settlement" simply means that an order for a transfer goes directly from the requesting bank to the paying bank instead of going though various "correspondent" banks to exchange money, convert currency, etc. It's naturally quicker and less costly. The characterizations as "kind of like SWIFT on steroids" is misleading as though the real difference is other than direct bi-lateral currency settlement. The technological advantages, if any, are due to CIPS being invented and implemented more recently and thus are using current technology. But, that fact also misleads because the SWIFT system, while comparatively aged, is constantly upgrading and has the same tech available to that system as CIPS.

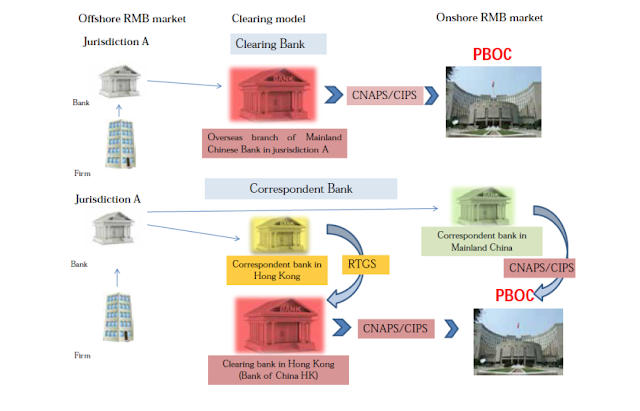

This is a decent illustration on how the CIPS system was designed to work:

Alright, now armed with a little information, perhaps the "mystical" aspect of CIPS can be put aside and an honest look taken at how the world can get heretofore unknown riches infused. Remember, this is not even talking about the implications of such an unspeakably massive infusion of funds into the world's financial structures. That's another story and debate.

Blockchain technologies? At its core, this is merely technology for thousands or even millions of computers across the planet to jointly manage the database that records transactions of cryptocurrencies or bank account balances. The primary point of security is that no single person or bank controls what "written" on someone's (or everyone's) bank account balance sheet. This easily translates into transferring funds between institutions/banks.

fireswain does what techs do, they talk about lots of very real and truthful stuff but at a level of relevance interesting only to those who code the program or diagram it out for planning and functionality. How great it would be if we each acknowledged our respective expertise! I am not a computer expert despite building lots of small networks and countless small business computer towers as a hobbie. All it takes is a little reading. The above is a simple and excellent example of what's available for anyone to get to know that cares to.

The seemingly mysterious and convoluted process described by fireswain is actually a decent explanation from "down in the weeds" with about 400% more detail than functionally necessary to describe what "Kim" or anyone needs to do to transfer massive funds. The dinarland shorthand for so many things has created confusion and a needlessly "mystical" feeling to this very real and very manageable banking action. Of course, not everyone will know and understand it. Not everyone has "hundreds of quintillions of dollars" to divvy up to the world, but it IS just a step by step banking procedure that, on a MUCH smaller scale, I've done done myself.

So come on.... there's been no "gotcha" moment or facts which can in any rational way be used to discredit "Kim". Be clear, I am not an apologist for "Kim". I've sought to speak with her and been blocked in just about every practical way by Tank and his blog lieutenant. So, I'm not "buddies" with her and covering her here. I just don't like the "piling on" by use of either cool tech talk or just basic character assassination. What she has said just rings true if you weren't looking for a whitepaper on the deep tech CIPS uses or the procedural manual for every conceivable transaction "Kim" might initiate. How silly.

How about a decent and honest conversation. The one-ups-manship is unprofessional and certainly not fitting to people who might end up trillionaires.

One last point about the dismissal and discarding of "Kim". Much was said about "what we've been told" and "the way they explained things are". Has anyone thought that maybe, just maybe, about as much of was told to us about "the way things are" as have been true of the "800#" releases? In other words, it's at least as likely as not that the foundation against which you have recently measured the "truth" or "accuracy" or "reliability" of "Kim" is simply false (no matter how well sold to us or how long browbeaten into us as a currency community by gurus who have come and failed and gone).

Stubbornly grounded,

I am,

ubiety

[Preface: Sorry in advance for typos and whatever else results from my haste. I'm trying to squeeze this in before an appointment in my actual business because the resistance among some exotic currency holders to very self-exposed help is troubling. I appreciate your indulgence.]

I realize fireswain [sic] is your new tech guru here in IDC, however, let's be clear, this person is a tech. She loves tech, she love to talk tech, she loves to impress with tech, but don't misunderstand - she is a tech not a designer of SWIFT, CIPS, or any of these long standing and fully public technologies.

Background on SWIFT, available to all of us:

SWIFT, or the Society for Worldwide Interbank Financial Telecommunication, is the world’s largest electronic payment messaging system, facilitating the exchange of more than $6 trillion a day, according to 2012 estimates. Though it gets lumped in with electronic funds transfer systems, it doesn’t do any of the funds transfers itself. In fact, it doesn’t even touch money. It does make money move by triggering the transfer mechanism between correspondent banks.

At its core, SWIFT is basically just a bank-to-bank messaging system. It supplies a standardized language that institutions use to communicate payment instructions and other info to each other. SWIFT messages are programmed in a language known as FIN. The system was designed and used to transfer messages between member institutions.

Before SWIFT, there was Telex. It’s helpful to start there, because rather than being created from scratch, the SWIFT system is rooted in some precedent. Telex—or the Teleprinter exchange, if we’re getting formal—was (and is) one of the original ways to transmit data developed during World War II. Though its roots were in the military, it was quickly adopted by financial institutions for their systems to communicate internationally.

By the 70s, Telex had gotten old: It was indisputably slow (transmitting bytes per second), lacked formatting standards (limiting the possibility to automate), and wasn’t as secure as evolving threats demanded (after all, it had basically become a directory served over the phone networks). Around the same time, domestic electronic funds transfer systems began to emerge, driven by a desire to eliminate paper from the payments process. (Imagine: the push to go paperless was a process that took shape in the 60s.) The distinction, of course, is that EFTs actually move money. But they often used Telex messages to get information about what needed to happen—which made the issues with Telex all the more pointed.

So in 1973, after a handful of studies and a lot of talking, a group of banks established SWIFT as a specialist’s alternative to Telex. They selected Brussels for the cooperative’s headquarters—evidently, choosing New York or London would have been too political. By the time SWIFT went live three years later, it comprised a messaging platform, a computer system to validate and route messages, and a set of message standards. More than 500 institutions from 22 countries were connected. Today, more than 11,000 institutions in more than 200 nations are connected to SWIFT. In 2015 alone, 6.1 billion FIN messages were sent through the network.

Here's a basic diagram on how SWIFT actually works.

SWIFT uses a system of codes to detail where a transfer is coming from, where it’s going, and how it’ll to get there. These strings of alphanumeric identifiers comprise an institution code, a country code, a location code, and a branch code. So in that way, it’s not dissimilar to the U.S. routing number system.

It’s worth reiterating that, because SWIFT doesn’t actually send money, institutions that use the network also need banking relationship to move funds. Each financial institution will have a dedicated SWIFT interface (in other words, a computer-based terminal) on-premises. Most banks set up their SWIFT systems so that they’re isolated from the rest of their networks. (Though, again, as we’ll cover later, not all do.)

Users can log in to these terminals to manually enter messages. Messages can also be auto-generated by the institution’s computer system and passed on to the terminal. The terminal then sends the SWIFT message to the regional processors in the sender’s country. The terminals only connect with processors through leased line, dial up, or public data network connections.

From there, the regional processor checks, stores, and forwards the data to its operating center, which passes the message on to the processor in the recipient’s country. That processor delivers the message to the receiver’s terminal, and then sends confirmation. Officials at the respective financial institutions are supposed to audit these to prevent fraud.

As indicated above, actually transferring funds internationally is a bank matter. Say two customers of the same bank are located in two different countries and want to transfer funds. The customer in country A will ask the bank to transfer funds to the customer in country B. Branch A will then tell its counterpart what to do via SWIFT. And then it’ll wire the funds and make the required book entries in its accounting system. That’s it. But it’s usually more complicated than that, and it often involves more financial institutions.

For example, if one financial institution doesn’t even have a branch in the beneficiary’s country, it might need to loop other institutions—in this context, called correspondent banks—to complete the transaction. If both banks (conveniently!) maintain accounts at a third institution, they might use that third bank to expedite things. They’d identify the relationship, send a secure message over SWIFT between the banks, and do a book transfer.

CIPS, also publicly available information:

One has to first understand the CIPS initiative before looking into how it works. The Cross-border Inter-bank Payments system is designed to facilitate financial transactions between different countries. To be more specific, the entire network settles cross-border RMB (Chinese currency) payments and trade for all of its partners. This means China is taking center-stage as far as this payments platform is concerned.

The development of CIPS dates back all the way to several years ago. After a few years of development, the first phase of CIPS was introduced to the rest of the world. The project gained immediate support from 19 Chinese and foreign banks, as well as 176 indirect participants across 6 different countries. At that time, some people saw it as a way for Russia and China to develop a payment system that could rival with SWIFT.

However, it appears that is not necessarily the goal, as CIPS signed a Memorandum of Understanding with SWIFT in 2016. To be more specific, SWIFT would be used as a secure and efficient communication tool for CIPS’s connection with established members. In a way, this is meant to allow cross-platform compatibility between different payment networks, as there is no reason to think CIPS wants to directly compete with SWIFT in the West.

It is also worth mentioning CIPS is not designed to facilitate funds transfer, as it is designed to send payment orders to be settled by correspondent accounts (keep this in mind every time you read someone talking about CIPS transferring money). This means partners of CIPS must have a banking relationship by either being a bank themselves or affiliating with an existing financial institution. It is not open to just anyone by any means, yet it aims to speed up cross-border payments by quite a margin. Or that is how it was supposed to go until things came to a change back in 2015.

To put this latter part into perspective, the CIPS protocol serves as a cross-border yuan trade deal tool instead of a network designed to facilitate capital-related transfers. Providing a unified network for settling deals in yuan sounds great on paper, yet the idea has suffered some setbacks in the past few years. The 2015 Chinese stock market crash has not helped matters either.

CIPS v SWIFT is about clearing – not investment money and it has no impact upon parking (i.e., storing or safekeeping) money. CIPS platforms which functions for the RMB, the same way SWIFT does for the dollar. Yet unlike the way SWIFT charges for swaps when nations have to use the dollar as a middleman since it still reigns as the world's singular reserve currency, CIPS allows for much lower transaction fees and the convenience of bypassing the U.S. currency through direct bi-lateral currency settlement. This doesn't mean CIPS actually transfers the money, it simply works more closely with the "member" institutions which effect the actual transfer.

"Direct bi-lateral currency settlement" simply means that an order for a transfer goes directly from the requesting bank to the paying bank instead of going though various "correspondent" banks to exchange money, convert currency, etc. It's naturally quicker and less costly. The characterizations as "kind of like SWIFT on steroids" is misleading as though the real difference is other than direct bi-lateral currency settlement. The technological advantages, if any, are due to CIPS being invented and implemented more recently and thus are using current technology. But, that fact also misleads because the SWIFT system, while comparatively aged, is constantly upgrading and has the same tech available to that system as CIPS.

This is a decent illustration on how the CIPS system was designed to work:

Alright, now armed with a little information, perhaps the "mystical" aspect of CIPS can be put aside and an honest look taken at how the world can get heretofore unknown riches infused. Remember, this is not even talking about the implications of such an unspeakably massive infusion of funds into the world's financial structures. That's another story and debate.

Blockchain technologies? At its core, this is merely technology for thousands or even millions of computers across the planet to jointly manage the database that records transactions of cryptocurrencies or bank account balances. The primary point of security is that no single person or bank controls what "written" on someone's (or everyone's) bank account balance sheet. This easily translates into transferring funds between institutions/banks.

fireswain does what techs do, they talk about lots of very real and truthful stuff but at a level of relevance interesting only to those who code the program or diagram it out for planning and functionality. How great it would be if we each acknowledged our respective expertise! I am not a computer expert despite building lots of small networks and countless small business computer towers as a hobbie. All it takes is a little reading. The above is a simple and excellent example of what's available for anyone to get to know that cares to.

The seemingly mysterious and convoluted process described by fireswain is actually a decent explanation from "down in the weeds" with about 400% more detail than functionally necessary to describe what "Kim" or anyone needs to do to transfer massive funds. The dinarland shorthand for so many things has created confusion and a needlessly "mystical" feeling to this very real and very manageable banking action. Of course, not everyone will know and understand it. Not everyone has "hundreds of quintillions of dollars" to divvy up to the world, but it IS just a step by step banking procedure that, on a MUCH smaller scale, I've done done myself.

So come on.... there's been no "gotcha" moment or facts which can in any rational way be used to discredit "Kim". Be clear, I am not an apologist for "Kim". I've sought to speak with her and been blocked in just about every practical way by Tank and his blog lieutenant. So, I'm not "buddies" with her and covering her here. I just don't like the "piling on" by use of either cool tech talk or just basic character assassination. What she has said just rings true if you weren't looking for a whitepaper on the deep tech CIPS uses or the procedural manual for every conceivable transaction "Kim" might initiate. How silly.

How about a decent and honest conversation. The one-ups-manship is unprofessional and certainly not fitting to people who might end up trillionaires.

One last point about the dismissal and discarding of "Kim". Much was said about "what we've been told" and "the way they explained things are". Has anyone thought that maybe, just maybe, about as much of was told to us about "the way things are" as have been true of the "800#" releases? In other words, it's at least as likely as not that the foundation against which you have recently measured the "truth" or "accuracy" or "reliability" of "Kim" is simply false (no matter how well sold to us or how long browbeaten into us as a currency community by gurus who have come and failed and gone).

Stubbornly grounded,

I am,

ubiety

*****************

>>>TNTBS's YouTube Channel<<<

Ssmith- GURU HUNTER

- Posts : 20495

Join date : 2012-04-10

Re: "Kim, CIPS, SWIFT, Easing up!" by ubiety 1/26/18

![]() by Kevind53 Sat Jan 27, 2018 10:51 pm

by Kevind53 Sat Jan 27, 2018 10:51 pm

Well let's keep it simple Kim is a liar, Tank is a liar, his lieutenants are liars, and you are no better.

*****************

Trust but Verify --- R Reagan

"Rejoice always, pray without ceasing, in everything give thanks; for this is the will of God in Christ Jesus for you."1 Thessalonians 5:14–18

Kevind53- Super Moderator

- Posts : 27254

Join date : 2011-08-09

Age : 24

Location : Umm right here!

Page 1 of 1

Permissions in this forum:

You cannot reply to topics in this forum

» Phony Tony sez: Full Steam Ahead!

» Dave Schmidt - Zim Notes for Purchase (NOT PHYSICAL NOTES)

» Russia aren't taking any prisoners

» Deadly stampede could affect Iraq’s World Cup hopes 1/19/23

» ZIGPLACE

» CBD Vape Cartridges

» Classic Tony is back

» THE MUSINGS OF A MADMAN

» Minister of Transport: We do not have authority over any airport in Iraq

» Did Okie Die?

» Hello all, I’m new

» The Renfrows: Prophets for Profits, Happy Anniversary!

» What Happens when Cancer is treated with Cannabis? VIDEO

» An Awesome talk between Tucker and Russell Brand

» Trafficking in children

» The second American Revolution has begun, God Bless Texas

» The Global Currency Reset Evolution Event Will Begin With Gold, Zimbabwe ZWR Old Bank Notes

» Tucker talking Canada

» Almost to the end The goodguys are winning