Latest topics

Dave Schmidt (Meta 1 Coin) Workshop - Austrailia Requires Financial Services (AFS) licence - Ooops!

Page 1 of 1

Dave Schmidt (Meta 1 Coin) Workshop - Austrailia Requires Financial Services (AFS) licence - Ooops!

Dave Schmidt (Meta 1 Coin) Workshop - Austrailia Requires Financial Services (AFS) licence - Ooops!

![]() by RamblerNash Thu Sep 05, 2019 3:06 am

by RamblerNash Thu Sep 05, 2019 3:06 am

Will Dave Schmidt have another misinterpretation of the law event? LOL

~~~~~~~~~~

Initial coin offerings and crypto-assets

This information sheet (INFO 225) will help you to understand your obligations under the Corporations Act 2001 (Corporations Act) and the Australian Securities and Investments Commission Act 2001 (ASIC Act) if:

INFO 225 also refers to the Australian Consumer Law. However, it does not cover Australian legislation administered by other regulators who oversee ICOs and crypto-assets – such as the Australian Transaction Reports and Analysis Centre (AUSTRAC) and the Australian Taxation Office (ATO).

This information sheet answers the following questions:

For a discussion of distributed ledger technology see Information Sheet 219 Evaluating distributed ledger technology (INFO 219).

This information sheet will help you to understand your obligations under the Corporations Act and ASIC Act. Figure 1 provides high-level regulatory signposts for crypto-asset participants as a starting point.

If you are issuing crypto-assets such as tokens that fall within the definition of a ‘financial product’, Australian laws apply, including the requirement to hold an Australian financial services (AFS) licence: see Part C and for more information Regulatory Guide 1 AFS Licensing Kit: Part 1 – Applying for and varying an AFS licence (RG 1).

If you are issuing crypto-assets such as tokens that fall within the definition of a ‘financial product’, Australian laws apply, including the requirement to hold an Australian financial services (AFS) licence: see Part C and for more information Regulatory Guide 1 AFS Licensing Kit: Part 1 – Applying for and varying an AFS licence (RG 1).

If you are giving advice, dealing, or providing other intermediary services for crypto-assets that are financial products a range of Australian laws apply, including the requirement to hold an AFS licence: see Part C and for more information Regulatory Guide 36 Licensing: Financial product advice and dealing (RG 36).

If you are giving advice, dealing, or providing other intermediary services for crypto-assets that are financial products a range of Australian laws apply, including the requirement to hold an AFS licence: see Part C and for more information Regulatory Guide 36 Licensing: Financial product advice and dealing (RG 36).

Where miners and transaction processors are part of the clearing and settlement (CS) process for tokens that are financial products Australian laws apply: see Regulatory Guide 211 Clearing and settlement facilities: Australian and overseas operators (RG 211).

Where miners and transaction processors are part of the clearing and settlement (CS) process for tokens that are financial products Australian laws apply: see Regulatory Guide 211 Clearing and settlement facilities: Australian and overseas operators (RG 211).

If the platform deals in crypto-assets that are financial products, then the platform is operating a market and a range of Australian laws apply, including the requirement to hold an Australian market licence: see Part D and for more information Regulatory Guide 172 Financial markets: Domestic and overseas operators (RG 172). Depending on how transactions in crypto-assets that are financial products are cleared and/or settled, the platform may also be operating a CS facility and require a CS facility licence: see RG 211.

If the platform deals in crypto-assets that are financial products, then the platform is operating a market and a range of Australian laws apply, including the requirement to hold an Australian market licence: see Part D and for more information Regulatory Guide 172 Financial markets: Domestic and overseas operators (RG 172). Depending on how transactions in crypto-assets that are financial products are cleared and/or settled, the platform may also be operating a CS facility and require a CS facility licence: see RG 211.

If the payment service involves a ‘non-cash payment facility’ a range of Australian laws apply, including the requirement to hold an AFS licence: see Part C and for more information Regulatory Guide 185 Non-cash payment facilities (RG 185).

If the payment service involves a ‘non-cash payment facility’ a range of Australian laws apply, including the requirement to hold an AFS licence: see Part C and for more information Regulatory Guide 185 Non-cash payment facilities (RG 185).

If tokens stored by your business fall within the definition of a ‘financial product’, you need to ensure you hold the appropriate custodial and depository authorisations: see RG 1.

If tokens stored by your business fall within the definition of a ‘financial product’, you need to ensure you hold the appropriate custodial and depository authorisations: see RG 1.

If you are an individual or institution interested in participating in ICOs and acquiring crypto-assets, you can read information and warnings about ICOs on ASIC’s MoneySmart website.

If you are an individual or institution interested in participating in ICOs and acquiring crypto-assets, you can read information and warnings about ICOs on ASIC’s MoneySmart website.

You must not engage in misleading or deceptive conduct in the course of your business whether a financial product is involved or not: see Part B.

You must not engage in misleading or deceptive conduct in the course of your business whether a financial product is involved or not: see Part B.

Our experience suggests that ICOs by their nature seek to raise capital from the public to fund a particular project through the issue of crypto-assets such as tokens. If the crypto-asset issued by the ICO is a financial product (such as an interest in a managed investment scheme or a security), the issuer will need to consider the relevant capital raising provisions of the Corporations Act, AFS licensing requirements and other regulatory requirements. These regulatory requirements are in place to maintain the integrity of Australia’s financial market and ensure consumer protection.

For more information to help you in answering this question see Parts C, D and E.

Entities are expected to know who their investors are to justify a conclusion that exemptions under the Corporations Act for ‘wholesale’ or ‘sophisticated’ investors versus retail investors apply to the offering.

Whether or not a financial product is involved, promoters must always ensure that the ICO does not involve misleading or deceptive conduct or statements. Entities can do so by seeking professional advice (including legal advice) on all the facts and circumstances of the issue or sale of the ICO, not just a part of the sale.

As the design of the ICO or the crypto-asset can change over the course of the product development life cycle, entities are expected to seek professional advice and ensure ongoing compliance with the law. For example, it is particularly important to ensure that ongoing disclosures are kept up to date – failure to do so will increase the risk that the offer of the ICO, the ongoing issue of the crypto-asset and/or the information the issuer has provided about the ICO or crypto-asset could mislead or deceive consumers. See Part B for more information about what misleading or deceptive conduct is in relation to an ICO or crypto-asset.

Examples of other general Corporations Act requirements that will often apply include an officer’s duty to act in the best interests of a corporation or discharge their duties for a proper purpose.

Care should be taken to ensure promotional communications about a crypto-asset or ICO do not mislead or deceive potential consumers and do not contain false information.

Conduct that may be misleading or deceptive to consumers can include:

We have been delegated powers from the ACCC to, in coordination with the ACCC, respond to potentially misleading or deceptive conduct relating to crypto-assets which affect Australian consumers.

Regulatory Guide 234 Advertising financial products and services (including credit): Good practice guidance (RG 234) contains guidance to help businesses comply with their legal obligations not to make false or misleading statements or engage in misleading or deceptive conduct.

CSF intermediaries operate a platform through which start-ups and small businesses can raise up to $5 million. The capital is generally raised from a large number of consumers who invest small amounts of money in return for the issue of shares. Under the Corporations Act, acting as a CSF intermediary is a ‘financial service’ and specific laws apply to both the CSF intermediary as well as the companies seeking to make offers through the platform.

The laws require that a provider of CSF services must hold an AFS licence with authorisation to provide this service. This is not an exhaustive discussion of all the relevant Australian laws that apply in relation to providing CSF. It is the responsibility of the entities involved to ensure they comply with all relevant Australian laws.

The Corporations Act is likely to apply to an ICO that involves a financial product such as a managed investment scheme, security, derivative or non-cash payment (NCP) facility. This part discusses each of these financial products. Our experience suggests that many ICOs may be, or involve, interests in a managed investment scheme.

In some cases, ICO issuers may frame the entitlements received by contributors as a receipt for a purchased service. If the value of the crypto-assets acquired is affected by the pooling of funds from contributors, or the use of those funds under the arrangement, then the ICO is likely to be a managed investment scheme. This is particularly the case when the ICO is offered as an investment. Figure 2 can help in identifying whether an ICO is, or involves, a managed investment scheme.

There are a number of regulatory guides (such as Regulatory Guide 133 Funds management and custodial services: Holding assets (RG 133))that also set out obligations that are relevant to the operation of a retail managed investment scheme.

Failing to provide a PDS where required, providing a PDS that does not comply with specific content requirements under the Corporations Act or includes misleading or deceptive statements, may entitle investors who suffer loss or damage to obtain a refund of their investment amount or recover that loss or damage.

If an issuer of an ICO is operating a wholesale managed investment scheme they may need to obtain an AFS licence with the appropriate authorisations and must have a robust process to ensure that only wholesale clients invest in the managed investment scheme.

It is not permissible for the issuer, as trustee of the wholesale managed investment scheme, to rely on a corporate authorised representative appointment from another AFS licensee in order to issue interests in the scheme – as the issuer would not be ‘acting on behalf’ of the AFS licensee but rather issuing interests in the wholesale scheme as trustee in its own right. In addition, the issuer as trustee must ensure that any ‘white paper’, ‘lite paper’ or other promotional document issued in connection with the ICO does not include any misleading or deceptive statements – otherwise, investors who suffer loss or damage may be able to recover that loss or damage.

This is not an exhaustive discussion of all the relevant Australian laws that apply in relation to a managed investment scheme. It is the responsibility of the entities involved to ensure they comply with all relevant Australian laws.

If the scheme is not a managed investment scheme, it may involve a security or other financial product discussed below.

A share is a collection of rights relating to a company. There are a range of types of shares that may be issued. Most shares issued by companies that offer shares to the public are ‘ordinary shares’ and carry rights regarding the ownership of the company, voting rights in the decisions of the body, some entitlement to share in future profits through dividends, and a claim on the residual assets of the company if it is wound up.

Most shares issued in Australia come with the benefit to shareholders of limited liability as well.

The bundle of rights referred to above may be used to help determine if a token is in fact a security. If the rights attached to the crypto-asset (which are generally found in the ICO’s ‘white paper’ but may be found in other materials) are similar to rights commonly attached to a share – such as if there appears to be ownership of the body, voting rights in decisions of the body or some right to participate in profits of the body – then it is likely the crypto-asset is a share. If the crypto-asset gives the purchaser a right to acquire shares in the company at a time in the future (e.g. if it lists on the ASX) then this may be an option, which is also a security.

Australian laws apply

Where it appears that an issuer of an ICO is actually making an offer of a security, the issuer will generally need to prepare a prospectus. Such offers of securities that are shares are often described as initial public offerings (IPOs).

By law, a prospectus must contain all information that consumers reasonably require to make an informed investment decision. Generally, a prospectus should include audited financial information.

Importantly, though an ICO may look similar to an IPO, an ICO may not offer the same protections to consumers and may result in liability for the issuer and those involved in the ICO. Issuers of an ICO need to be aware that where an offer document for an ICO is, or should have been, a prospectus and that document does not contain all the information required by the Corporations Act, or includes misleading or deceptive statements, consumers may be able to withdraw their investment before the crypto-assets are issued or pursue the issuer and those involved in the ICO for the loss.

For more details about the information a prospectus should contain see Regulatory Guide 228 Prospectuses: Effective disclosure for retail investors (RG 228).

Offering, advising about, making a market for, providing custodial or depository services for, and dealing in, crypto-assets that are securities or other financial products may also attract specific AFS licensing requirements and other regulatory requirements.

This is not an exhaustive discussion of all the relevant Australian laws that apply in relation to an ICO offering a security. It is the responsibility of the entities involved to ensure they comply with all relevant Australian laws.

Australian laws apply

Where an issuer of an ICO is making an offer of a derivative to a retail investor, the issuer will need to prepare a PDS and comply with other regulatory requirements.

Services such as offering, advising about, making a market for, and dealing in, crypto-assets that are derivatives will also require an AFS licence.

This is not an exhaustive discussion of all the relevant Australian laws that apply in relation to an ICO involving a derivative. It is the responsibility of the entities involved to ensure they comply with all relevant Australian laws.

This type of facility can be a financial product which requires an AFS licence if payments can be made to more than one person. An intermediary that arranges for the issue of an NCP facility may need an AFS licence, or to act on behalf of an AFS licensee.

Australian laws apply

If an ICO involves an NCP facility an AFS licence may be needed. For general information on NCP facilities, including the low-value exemption that can apply, see RG 185.

This is not an exhaustive discussion of all the relevant Australian laws that apply in relation to an ICO that may involve an NCP facility. It is the responsibility of the entities involved to ensure they comply with all relevant Australian laws.

To operate in Australia, the platform operator will need to hold an Australian market licence unless covered by an exemption. There are currently no licensed or exempt platform operators in Australia that enable consumers to buy (or be issued) or sell crypto-assets that are financial products. Platform operators must not allow financial products to be traded on their platform without having the appropriate licence as this may amount to a significant breach of the law.

If so, the entities will be providing a financial service in issuing such financial products and may require a new AFS licence or licence variation (such as a new product authorisation).

For those entities that may want to apply for a new AFS licence or a licence variation:

Where a financial product is to be exchange-listed, we expect licensed Australian market operators will play an important gatekeeper role in ensuring the suitability of issuers and the products they are permitted to list and trade on their markets.

The definition of a financial product in Australia is often broader than in other jurisdictions. As such, crypto-assets such as utility tokens that may fall outside the regulatory perimeter in another jurisdiction may often be covered under our broader definition. It is important to always consider the particular rights and features of an individual ICO or crypto-asset in relation to Australian law to determine whether it is regulated as a financial product: see Part C.

For all inquiries, we strongly encourage entities to carefully consider their proposal and seek professional advice (including legal advice). In particular, we are not in a position to review a draft white paper and provide a view about the operation of Australian law in individual circumstances.

We do not provide any assessment or approval of an entity’s compliance with the law, including in relation to the business model adopted.

This is Information Sheet 225 (INFO 225) updated in May 2019. Information sheets provide concise guidance on a specific process or compliance issue or an overview of detailed guidance.

https://asic.gov.au/regulatory-resources/digital-transformation/initial-coin-offerings-and-crypto-assets/

~~~~~~~~~~

Initial coin offerings and crypto-assets

This information sheet (INFO 225) will help you to understand your obligations under the Corporations Act 2001 (Corporations Act) and the Australian Securities and Investments Commission Act 2001 (ASIC Act) if:

- you are considering raising funds through an initial coin offering (ICO), or

- your business is involved with crypto-assets such as cryptocurrency, tokens or stable coins.

INFO 225 also refers to the Australian Consumer Law. However, it does not cover Australian legislation administered by other regulators who oversee ICOs and crypto-assets – such as the Australian Transaction Reports and Analysis Centre (AUSTRAC) and the Australian Taxation Office (ATO).

This information sheet answers the following questions:

- Part A: What should you consider when offering crypto-assets through an ICO?

- Part B: What is misleading or deceptive conduct in relation to an ICO or crypto-asset?

- Part C: When could an ICO be or involve a financial product?

- Part D: When could a crypto-asset trading platform become a financial market?

- Part E: What about financial products that reference crypto-assets?

- Part F: How do overseas categorisations of crypto-assets translate to the Australian context?

- Part G: Where can I get more information?

For a discussion of distributed ledger technology see Information Sheet 219 Evaluating distributed ledger technology (INFO 219).

This information sheet will help you to understand your obligations under the Corporations Act and ASIC Act. Figure 1 provides high-level regulatory signposts for crypto-asset participants as a starting point.

Figure 1: Regulatory signposts for crypto-asset participants

Issuers of crypto-assets (e.g. tokens)

Crypto-asset intermediaries

Miners and transaction processors

Crypto-asset exchange and trading platforms

Crypto-asset payment and merchant service providers

Wallet providers and custody service providers

Consumers

Part A: What should you consider when offering crypto-assets through an ICO?

This part provides a non-exhaustive list of items to consider when offering an ICO.Is the crypto-asset issued by your ICO a financial product (or does it involve a financial product)?

Entities and their advisers need to consider all the rights and features of the ICO (regardless of how it is named and marketed) in determining whether the crypto-asset is a financial product or involves a financial product.Our experience suggests that ICOs by their nature seek to raise capital from the public to fund a particular project through the issue of crypto-assets such as tokens. If the crypto-asset issued by the ICO is a financial product (such as an interest in a managed investment scheme or a security), the issuer will need to consider the relevant capital raising provisions of the Corporations Act, AFS licensing requirements and other regulatory requirements. These regulatory requirements are in place to maintain the integrity of Australia’s financial market and ensure consumer protection.

For more information to help you in answering this question see Parts C, D and E.

If you do not consider your crypto-asset to be a financial product, can you substantiate your conclusion?

Entities should be prepared to justify a conclusion that their ICO does not involve a regulated financial product.Entities are expected to know who their investors are to justify a conclusion that exemptions under the Corporations Act for ‘wholesale’ or ‘sophisticated’ investors versus retail investors apply to the offering.

Are you complying with all relevant Australian laws on an ongoing basis?

Entities need to ensure that they comply with all the relevant Australian laws. This includes ensuring that all the information they provide to consumers, regardless of the media they use, complies with relevant laws including the Corporations Act, ASIC Act and the Australian Consumer Law, as well as anti-money laundering (AML) and know your client (KYC) obligations.Whether or not a financial product is involved, promoters must always ensure that the ICO does not involve misleading or deceptive conduct or statements. Entities can do so by seeking professional advice (including legal advice) on all the facts and circumstances of the issue or sale of the ICO, not just a part of the sale.

As the design of the ICO or the crypto-asset can change over the course of the product development life cycle, entities are expected to seek professional advice and ensure ongoing compliance with the law. For example, it is particularly important to ensure that ongoing disclosures are kept up to date – failure to do so will increase the risk that the offer of the ICO, the ongoing issue of the crypto-asset and/or the information the issuer has provided about the ICO or crypto-asset could mislead or deceive consumers. See Part B for more information about what misleading or deceptive conduct is in relation to an ICO or crypto-asset.

Examples of other general Corporations Act requirements that will often apply include an officer’s duty to act in the best interests of a corporation or discharge their duties for a proper purpose.

Part B: What is misleading or deceptive conduct in relation to an ICO or crypto-asset?

This part discusses when laws prohibiting misleading or deceptive conduct, or the Corporations Act, would apply to an ICO or crypto-asset.Misleading or deceptive conduct

Australian law prohibits misleading or deceptive conduct in a range of circumstances, including in trade or commerce, in connection with financial services, and in relation to a financial product. Australian laws and regulations that prohibit misleading or deceptive conduct may apply even if an interest in an ICO or crypto-asset is issued, traded or sold offshore. It is a serious breach of Australian law to engage in misleading or deceptive conduct.Care should be taken to ensure promotional communications about a crypto-asset or ICO do not mislead or deceive potential consumers and do not contain false information.

ICOs and crypto-assets that are not financial products

For ICOs and crypto-assets that are not financial products, the same prohibitions against misleading or deceptive conduct apply under the Australian Consumer Law. The Australian Competition and Consumer Commission (ACCC)’s Advertising and selling guide provides guidance on how to ensure advertising complies with the Australian Consumer Law.Conduct that may be misleading or deceptive to consumers can include:

- stating or conveying the impression that the ICO or crypto-assets (such as coins or tokens) offered are not a financial product if that is not the case

- stating or conveying the impression that a crypto-asset trading platform does not quote or trade financial products if that is not the case

- using social media to generate the appearance of a greater level of public interest in an ICO or crypto-asset

- undertaking or arranging for a group to engage in trading strategies to generate the appearance of a greater level of buying and selling activity for an ICO or crypto-asset

- failing to disclose adequate information about the ICO or crypto-asset, or

- suggesting that the ICO or crypto-asset is a regulated product or the regulator has approved the ICO or crypto-asset if that is not the case.

We have been delegated powers from the ACCC to, in coordination with the ACCC, respond to potentially misleading or deceptive conduct relating to crypto-assets which affect Australian consumers.

ICOs and crypto-assets that are financial products

For ICOs and crypto-assets that are financial products, the ASIC Act and the Corporations Act include prohibitions against misleading or deceptive conduct.Regulatory Guide 234 Advertising financial products and services (including credit): Good practice guidance (RG 234) contains guidance to help businesses comply with their legal obligations not to make false or misleading statements or engage in misleading or deceptive conduct.

What is the relationship between ICOs and crowd-sourced funding?

ICOs are sometimes referred to by industry as a form of crowd funding. Crowd funding using an ICO is not the same as ‘crowd-sourced funding’ (CSF) regulated by the Corporations Act. Care should be taken to ensure the public is not misled about the application of the CSF laws to an ICO. There are specific laws for the CSF regime which reduce the regulatory requirements for public fundraising while maintaining appropriate investor protection measures.CSF intermediaries operate a platform through which start-ups and small businesses can raise up to $5 million. The capital is generally raised from a large number of consumers who invest small amounts of money in return for the issue of shares. Under the Corporations Act, acting as a CSF intermediary is a ‘financial service’ and specific laws apply to both the CSF intermediary as well as the companies seeking to make offers through the platform.

The laws require that a provider of CSF services must hold an AFS licence with authorisation to provide this service. This is not an exhaustive discussion of all the relevant Australian laws that apply in relation to providing CSF. It is the responsibility of the entities involved to ensure they comply with all relevant Australian laws.

- More about the CSF regime

Part C: When could an ICO be or involve a financial product?

This part considers types of ICO offers made available to consumers in Australia and whether the Corporations Act might apply to them. It answers the following questions:- When could an ICO be a managed investment scheme?

- When could an ICO be an offer of a security?

- When could an ICO be an offer of a derivative?

- When could the coin issued under an ICO be a non-cash payment facility?

The Corporations Act is likely to apply to an ICO that involves a financial product such as a managed investment scheme, security, derivative or non-cash payment (NCP) facility. This part discusses each of these financial products. Our experience suggests that many ICOs may be, or involve, interests in a managed investment scheme.

Rights attached to crypto-assets

The rights attached to the crypto-assets issued under an ICO are a key consideration in assessing its legal status as a financial product. These rights are generally described in the ICO’s ‘white paper’, an offer document issued by the business making the offer or sale of an ICO crypto-asset. Rights may also be determined from other circumstances (e.g. how the ICO or crypto-asset is marketed to investors). What is a ‘right’ should be interpreted broadly. Rights that may arise in the future or on a contingency, and rights that are not legally enforceable, are included.When could an ICO be a managed investment scheme?

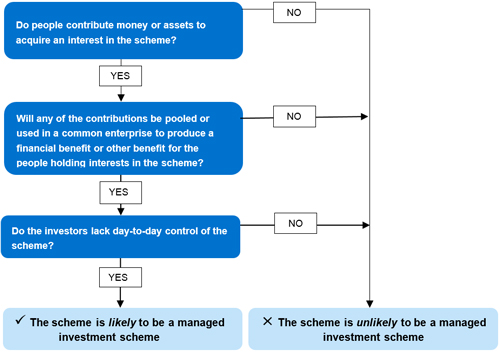

What is a managed investment scheme?

A managed investment scheme is a form of collective investment vehicle. It is defined in the Corporations Act and has three elements:- people contribute money or assets (such as cryptocurrency or other crypto-assets) to obtain an interest in the scheme (subject to limited exceptions, ‘interests’ in a scheme are generally a type of ‘financial product’ and are regulated by the Corporations Act)

- any of the contributions are pooled or used in a common enterprise to produce financial benefits or interests in property (e.g. using funds raised from contributors to develop the platform), for purposes that include producing a financial benefit for contributors (e.g. from an increase in the value of their tokens), and

- the contributors do not have day-to-day control over the operation of the scheme but, at times, may have voting rights or similar rights.

Application to ICOs

As noted above, what is a ‘right’ should be interpreted broadly. If the rights and value of the crypto-asset are related to an arrangement with the three elements described above, the crypto-asset issuer is likely to be offering interests in a managed investment scheme.In some cases, ICO issuers may frame the entitlements received by contributors as a receipt for a purchased service. If the value of the crypto-assets acquired is affected by the pooling of funds from contributors, or the use of those funds under the arrangement, then the ICO is likely to be a managed investment scheme. This is particularly the case when the ICO is offered as an investment. Figure 2 can help in identifying whether an ICO is, or involves, a managed investment scheme.

Figure 2: Is the ICO a managed investment scheme?

Australian laws apply

If an issuer of an ICO is operating a retail managed investment scheme offered to retail investors they will need to:- register the scheme with ASIC

- establish a constitution and compliance plan

- obtain an AFS licence to act as a responsible entity, and

- prepare and issue a compliant product disclosure statement (PDS), and comply with other disclosure obligations.

There are a number of regulatory guides (such as Regulatory Guide 133 Funds management and custodial services: Holding assets (RG 133))that also set out obligations that are relevant to the operation of a retail managed investment scheme.

Failing to provide a PDS where required, providing a PDS that does not comply with specific content requirements under the Corporations Act or includes misleading or deceptive statements, may entitle investors who suffer loss or damage to obtain a refund of their investment amount or recover that loss or damage.

If an issuer of an ICO is operating a wholesale managed investment scheme they may need to obtain an AFS licence with the appropriate authorisations and must have a robust process to ensure that only wholesale clients invest in the managed investment scheme.

It is not permissible for the issuer, as trustee of the wholesale managed investment scheme, to rely on a corporate authorised representative appointment from another AFS licensee in order to issue interests in the scheme – as the issuer would not be ‘acting on behalf’ of the AFS licensee but rather issuing interests in the wholesale scheme as trustee in its own right. In addition, the issuer as trustee must ensure that any ‘white paper’, ‘lite paper’ or other promotional document issued in connection with the ICO does not include any misleading or deceptive statements – otherwise, investors who suffer loss or damage may be able to recover that loss or damage.

This is not an exhaustive discussion of all the relevant Australian laws that apply in relation to a managed investment scheme. It is the responsibility of the entities involved to ensure they comply with all relevant Australian laws.

If the scheme is not a managed investment scheme, it may involve a security or other financial product discussed below.

- More about funds management

When could an ICO be an offer of a security?

What is a security?

The most common type of security is a share. An option to acquire a share by way of issue is considered to be a ‘security’ under the Corporations Act. For example, if the product being offered gives the right to be issued shares in the future, it may be an option. A debenture is also considered to be a ‘security’ under the Corporations Act. Debentures are a way for businesses to raise money from investors. In return for money, the business issuing the debenture promises to pay the investor interest, and the money lent to the business by the investor, at a future date.A share is a collection of rights relating to a company. There are a range of types of shares that may be issued. Most shares issued by companies that offer shares to the public are ‘ordinary shares’ and carry rights regarding the ownership of the company, voting rights in the decisions of the body, some entitlement to share in future profits through dividends, and a claim on the residual assets of the company if it is wound up.

Most shares issued in Australia come with the benefit to shareholders of limited liability as well.

- More about shares

Application to ICOs

When an ICO is created to fund a company (or to fund an undertaking that looks like a company) then the rights attached to the crypto-asset issued by the ICO may fall within the definition of a security – which includes a share or the option to acquire a share in the future.The bundle of rights referred to above may be used to help determine if a token is in fact a security. If the rights attached to the crypto-asset (which are generally found in the ICO’s ‘white paper’ but may be found in other materials) are similar to rights commonly attached to a share – such as if there appears to be ownership of the body, voting rights in decisions of the body or some right to participate in profits of the body – then it is likely the crypto-asset is a share. If the crypto-asset gives the purchaser a right to acquire shares in the company at a time in the future (e.g. if it lists on the ASX) then this may be an option, which is also a security.

Australian laws apply

Where it appears that an issuer of an ICO is actually making an offer of a security, the issuer will generally need to prepare a prospectus. Such offers of securities that are shares are often described as initial public offerings (IPOs).

By law, a prospectus must contain all information that consumers reasonably require to make an informed investment decision. Generally, a prospectus should include audited financial information.

Importantly, though an ICO may look similar to an IPO, an ICO may not offer the same protections to consumers and may result in liability for the issuer and those involved in the ICO. Issuers of an ICO need to be aware that where an offer document for an ICO is, or should have been, a prospectus and that document does not contain all the information required by the Corporations Act, or includes misleading or deceptive statements, consumers may be able to withdraw their investment before the crypto-assets are issued or pursue the issuer and those involved in the ICO for the loss.

For more details about the information a prospectus should contain see Regulatory Guide 228 Prospectuses: Effective disclosure for retail investors (RG 228).

Offering, advising about, making a market for, providing custodial or depository services for, and dealing in, crypto-assets that are securities or other financial products may also attract specific AFS licensing requirements and other regulatory requirements.

This is not an exhaustive discussion of all the relevant Australian laws that apply in relation to an ICO offering a security. It is the responsibility of the entities involved to ensure they comply with all relevant Australian laws.

- More about AFS licensing requirements

When could an ICO be an offer of a derivative?

What is a derivative?

Section 761D of the Corporations Act provides a broad definition of a derivative. For the purpose of this information sheet a ‘derivative’ is a product that derives its value from another ‘thing’ which is commonly referred to as the ‘underlying instrument’ or ‘reference asset’. The underlying instrument may be, for example, a share, a share price index, a pair of currencies or a commodity (including a crypto-asset).Application to ICOs

An ICO may involve a derivative if it involves a crypto-asset that is priced based on factors such as the price of another financial product, underlying market index or asset price moving in a certain direction before a time or event which resulted in a payment being required as part of the rights or obligations attached to the crypto-asset. For example, the crypto-asset could contain a self-executing contract involving payment arrangements that are triggered by changes in the relevant price of the underlying product, index or asset.Australian laws apply

Where an issuer of an ICO is making an offer of a derivative to a retail investor, the issuer will need to prepare a PDS and comply with other regulatory requirements.

Services such as offering, advising about, making a market for, and dealing in, crypto-assets that are derivatives will also require an AFS licence.

This is not an exhaustive discussion of all the relevant Australian laws that apply in relation to an ICO involving a derivative. It is the responsibility of the entities involved to ensure they comply with all relevant Australian laws.

- More about the licensing of derivatives

When could the coin issued under an ICO be a non-cash payment facility?

What is a non-cash payment facility?

A non-cash payment (NCP) facility is an arrangement through which a person makes payments, or causes payments to be made, other than by the physical delivery of currency.This type of facility can be a financial product which requires an AFS licence if payments can be made to more than one person. An intermediary that arranges for the issue of an NCP facility may need an AFS licence, or to act on behalf of an AFS licensee.

Application to ICOs

Crypto-assets such as tokens offered under an ICO are unlikely to be NCP facilities – though they may be a form of value that is used to make a payment (instead of physical currency). An ICO may involve an NCP facility if it includes an arrangement that allows:- payments to be made in this form of value to a number of payees, or

- payments to be started in this form and converted to fiat currency to enable completion of the payment.

Australian laws apply

If an ICO involves an NCP facility an AFS licence may be needed. For general information on NCP facilities, including the low-value exemption that can apply, see RG 185.

This is not an exhaustive discussion of all the relevant Australian laws that apply in relation to an ICO that may involve an NCP facility. It is the responsibility of the entities involved to ensure they comply with all relevant Australian laws.

Part D: When could a crypto-asset trading platform become a financial market?

This part provides guidance about platforms that enable trading of crypto-assets.What is a financial market?

A financial market is a facility through which offers to acquire or dispose of financial products are regularly made. Anyone who operates a financial market in Australia must obtain a licence to do so or otherwise be exempted by the Minister.Application to ICOs and crypto-assets

Where a crypto-asset is a financial product (whether it is an interest in a managed investment scheme, security, derivative or NCP facility), then any platform that enables consumers to buy (or be issued) or sell these crypto-assets may involve the operation of a financial market.To operate in Australia, the platform operator will need to hold an Australian market licence unless covered by an exemption. There are currently no licensed or exempt platform operators in Australia that enable consumers to buy (or be issued) or sell crypto-assets that are financial products. Platform operators must not allow financial products to be traded on their platform without having the appropriate licence as this may amount to a significant breach of the law.

- More about markets

Part E: What about financial products that reference crypto-assets?

Entities may propose to issue financial products that:- are linked to, or reference, crypto-assets

- invest in crypto-assets, or

- otherwise enable consumers to have exposure to crypto-assets.

If so, the entities will be providing a financial service in issuing such financial products and may require a new AFS licence or licence variation (such as a new product authorisation).

For those entities that may want to apply for a new AFS licence or a licence variation:

- we will assess the application under relevant policy and, based on our risk-targeted framework, take into account the considerations that apply to financial products of that type generally

- applications for crypto-asset-related financial products are more likely to be novel applications – our experience to date indicates that assessment of those applications may take more time, and

- we will work with businesses to identify the issues to be addressed in the application, and will issue additional guidance if we think that doing so may be helpful to industry.

Where a financial product is to be exchange-listed, we expect licensed Australian market operators will play an important gatekeeper role in ensuring the suitability of issuers and the products they are permitted to list and trade on their markets.

Part F: How do overseas categorisations of crypto-assets translate to the Australian context?

A number of international regulators have issued guidance on the application of their securities and financial services laws to ICOs and have defined the function of a range of crypto-assets (e.g. utility tokens and exchange tokens). These categorisations do not automatically translate to equivalent products in Australia.The definition of a financial product in Australia is often broader than in other jurisdictions. As such, crypto-assets such as utility tokens that may fall outside the regulatory perimeter in another jurisdiction may often be covered under our broader definition. It is important to always consider the particular rights and features of an individual ICO or crypto-asset in relation to Australian law to determine whether it is regulated as a financial product: see Part C.

Part G: Where can I get more information?

Entities that have specific requests or questions about an ICO or crypto-asset may contact our Innovation Hub or their existing ASIC contact. The Innovation Hub can help by providing tailored guidance to innovative businesses on how to access information and services relevant to them through the ASIC website.For all inquiries, we strongly encourage entities to carefully consider their proposal and seek professional advice (including legal advice). In particular, we are not in a position to review a draft white paper and provide a view about the operation of Australian law in individual circumstances.

We do not provide any assessment or approval of an entity’s compliance with the law, including in relation to the business model adopted.

Important note

The information in this publication should not be considered legal advice. You will need to obtain your own legal advice in relation to the applicable laws.Related information

- ASIC’s role and the laws we administer

- AFS licences

- ASIC’s Innovation Hub

- Investing in ICOs – ASIC’s MoneySmart website

This is Information Sheet 225 (INFO 225) updated in May 2019. Information sheets provide concise guidance on a specific process or compliance issue or an overview of detailed guidance.

https://asic.gov.au/regulatory-resources/digital-transformation/initial-coin-offerings-and-crypto-assets/

*****************

>>>TNTBS's YouTube Channel<<<

RamblerNash- GURU HUNTER

- Posts : 24270

Join date : 2015-02-19

Page 1 of 1

Permissions in this forum:

You cannot reply to topics in this forum

» Phony Tony sez: Full Steam Ahead!

» Dave Schmidt - Zim Notes for Purchase (NOT PHYSICAL NOTES)

» Russia aren't taking any prisoners

» Deadly stampede could affect Iraq’s World Cup hopes 1/19/23

» ZIGPLACE

» CBD Vape Cartridges

» Classic Tony is back

» THE MUSINGS OF A MADMAN

» Minister of Transport: We do not have authority over any airport in Iraq

» Did Okie Die?

» Hello all, I’m new

» The Renfrows: Prophets for Profits, Happy Anniversary!

» What Happens when Cancer is treated with Cannabis? VIDEO

» An Awesome talk between Tucker and Russell Brand

» Trafficking in children

» The second American Revolution has begun, God Bless Texas

» The Global Currency Reset Evolution Event Will Begin With Gold, Zimbabwe ZWR Old Bank Notes

» Tucker talking Canada

» Almost to the end The goodguys are winning